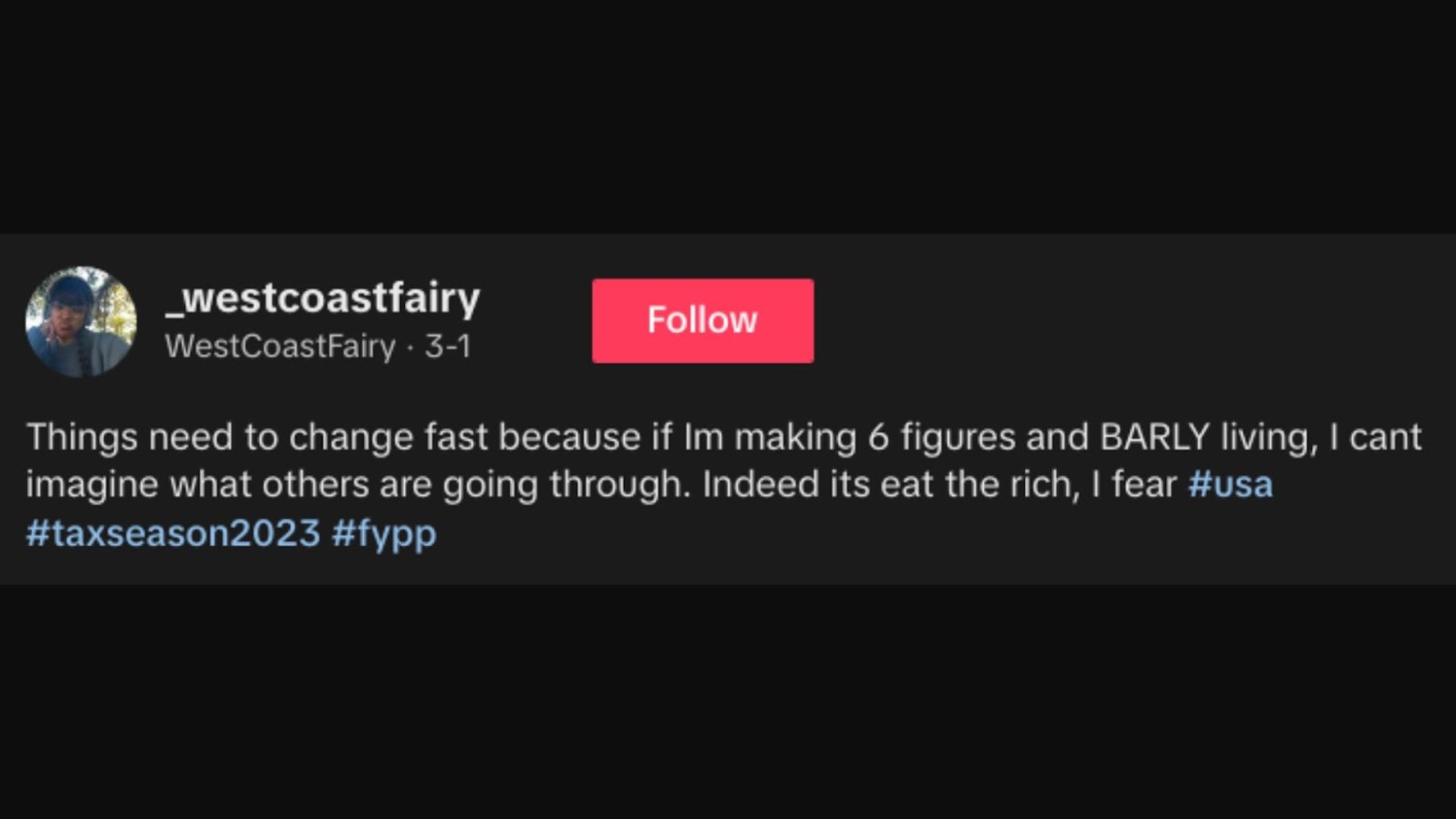

A California resident and new business owner recently uploaded a video to the popular social media platform TikTok regarding her 2023 taxes.

She told her viewers that, after filing her taxes, she was told she had to pay an almost unbelievable $26,000 in taxes after making $100,000 last year. Known as “WestCoastFairy,” this California TikToker says that’s more than her student loans, more than she has in the bank, and she has no idea what to do next.

The Viral Video

The TikTok video, which is now making headlines all over the country, was posted by 25-year-old WestCoastFairy on March 1, 2024. In it, she explains she has filed her taxes and is having extreme anxiety because she just realized she owes the federal government $18,000 and $8,000 to California. All because she made $100,00 as an independent contractor within her startup in 2023.

She captioned the video, “Things need to change fast because if I’m making 6 figures and BAR[E]LY living, I can’t imagine what others are going through. Indeed its eat the rich, I fear.”

What’s Going on Here?

In her video, WestCoastFairy says, “I literally can’t believe [it]… what is going on in America?” And there’s no doubt that any one of the millions who listened to this young entrepreneur’s tale is wondering the exact same thing: What is going on?

The first thing to note is that this extremely large total of $26,000 in annual taxes is not incorrect. In fact, some financial experts believe this may actually be the reduced number, thanks to the handiwork of a talented accountant.

Understanding the US Tax Brackets

Essentially, because WestCoastFairy made $100,000 as an independent contractor last year, she falls into four separate tax brackets. According to the Internal Revenue Service (IRS), she pays 10% on the first $11,000, 12% between $11,001 and $44,725, 22% from $33,726 to $95,375, and an almost unbelievable 24% between $95,376 and $100,000.

WestCoastFairy paid $18,000 in federal taxes, which was 17% of her income, meaning her federal dues were technically spot on.

Taxes in California

Now, regarding income taxes, it’s important to understand that each of the 50 states of America has its own regulations. California, for example, charges a 9.3% tax on anyone who makes between $68,351 and $349,137.

With an annual income of $100,000, WestCoastFairy falls into that category and would, therefore, have had to pay $9,300 in 2023. However, she only paid $8,000, hence the rumor that an accountant helped her save a bit through the process.

The TikToker Says She’s Frustrated by the Surprise

In her video, WestCoastFairy mentions that one of the most frustrating aspects of this situation is that she didn’t realize she was going to owe $26,000 at the end of the year. While she did save throughout the year, knowing she would owe something, she didn’t put away nearly that much.

When WestCoastFairy’s 2023 taxes were broken down, she only paid 26% of her annual income, whereas the majority of Americans pay about 30%. So some say she should have been prepared for such a large sum at the end of the year, but there’s a reason why she didn’t.

Starting a New Business Changes the Way One Pays Taxes

Essentially, that 30% is usually deducted, at least in part, from every paycheck of a standard employee. That means at the end of the year, one’s taxes don’t add up to tens of thousands because most of it has already been paid. However, many Americans don’t pay close attention to their paychecks.

Now, many Americans are abandoning the standard nine-to-five work week in favor of starting their own business. But the vast majority of these people don’t realize that by not paying taxes through their paychecks throughout the year, they’re in store for a huge bill in April.

Financial Experts Are Urging New Business Owners to Complete More Extensive Research

According to the US Census Bureau, nearly 5.5 million new businesses were created in the United States in 2023. Financial experts have now, more than ever, been urging new business owners to understand federal and state taxes before they open their doors.

Popular finance guru Dave Ramsey suggests to his viewers that any business owner or independent contractor should be saving at least 30% of each paycheck to use for their taxes at the end of the year.

WestCoastFairy Said She Did Save, Just not Enough

In her TikTok clip, WestCoastFairy explained she did save throughout the year in anticipation of her taxes, but it just wasn’t enough. Of course, if she had followed Ramsey’s advice, she would have $4,000 extra, but she hadn’t heard that trick of the trade before.

Additionally, the young entrepreneur explained she spent a significant percentage of her savings throughout the year on healthcare. She paid $10,000 for health insurance, as well as another $10,000 for out-of-pocket costs, none of which were tax deductible.

There Are Ways for New Business Owners to Cut Back on Healthcare Spending

Of the nearly 10,000 comments on WestCoastFairy’s video, many provided helpful tips and advice on how to cut back on healthcare costs this year.

A few noted that creating a Health-Savings Account (HSA) would drastically minimize both her healthcare costs and even her taxes at the end of the year.

The Right Accountant Is Important When Starting a New Business

It seems the bottom line for many Americans, including WestCoastFairy, is that they simply don’t know enough about their state and the federal taxation system to prepare for filing.

Therefore, even though it can be helpful to listen to financial experts on TikTok, YouTube, or their various podcasts, the best thing a new business owner can do for themselves is to hire an accountant to explain it all at the very beginning.

Is There Something Wrong With America’s Taxation System?

Many who commented on the video expressed their frustrations with US taxation policies, and others gave helpful advice for next year. Though one of the most poignant themes among the comments was that the system feels as though it was made to trick hard-working Americans.

The vast majority of Americans need to pay an accountant to do their taxes for them because the process is so pedantic and confusing. And many are now arguing that even if taxes are to sit at the percentages they do now, the system should not be too complex for the average person to understand.

Pros of Running a Small Business from a Tax Perspective

Small businesses enjoy unique tax advantages, such as the ability to write off various expenses—from equipment purchases to portions of home office utilities (via Investopedia).

Additionally, there are numerous tax credits designed specifically for small entities, which can significantly lower the overall tax burden. This creates a favorable environment for growth and reinvestment.

Cons of Running a Small Business from a Tax Perspective

Despite the benefits, small business owners face daunting tax responsibilities that can lead to significant stress and financial strain.

The complexity of tax laws may result in large, unexpected tax bills if not managed properly. Moreover, the burden of staying compliant with frequent tax law changes rests solely on the business owner.

Common Tax Deductions for Small Businesses

Effective tax management involves maximizing deductible expenses. Small businesses can deduct costs such as office supplies, travel expenses, and even meals (via Investopedia).

Additionally, capital expenses like machinery purchases can be depreciated over time, providing a substantial tax shield and helping to reduce taxable income annually.

Tax Credits Available to Small Businesses

To encourage growth, the government offers several tax credits to small businesses, including incentives for hiring employees, implementing environmentally friendly practices, and providing access to health insurance.

These credits not only reduce the amount of tax owed but can also improve a company’s bottom line.

Importance of Proper Accounting

Accurate accounting is the backbone of effective tax management. Keeping detailed records allows business owners to track every transaction, ensuring that nothing is overlooked during tax time.

This precision helps in claiming all entitled deductions and credits, ultimately reducing the overall tax liability.

Planning for Quarterly Estimated Taxes

For independent contractors and small business owners, paying quarterly estimated taxes is essential to avoid penalties.

These payments are an approximation of the tax liability for the year, based on income, dividends, and other taxable resources, helping to manage cash flow more effectively throughout the year.

The Role of a Professional Accountant

Hiring a professional accountant can be invaluable.

An accountant well-versed in small business taxation can provide strategic advice, ensure compliance with the latest tax laws, and optimize tax returns to take full advantage of all possible deductions and credits.

Utilizing Tax Software and Tools

Modern tax software, like Xero, offers comprehensive solutions that simplify the tax filing process for small businesses.

These tools can automate many aspects of tax preparation, from calculating deductions to filing returns electronically, ensuring accuracy and efficiency.

Legal Tax Saving Strategies

Implementing legal tax saving strategies like investing in retirement plans or setting up a Health Savings Account (HSA) can significantly reduce taxable income (via Investopedia).

These strategies not only provide immediate tax benefits but also contribute to the owner’s long-term financial security.

Avoiding Common Tax Pitfalls

Common pitfalls for small business owners include underestimating taxable income and poor record-keeping (via Cloud Friday Accounting).

Staying on top of your financial activities and keeping abreast of tax law changes are crucial steps in avoiding these issues, ensuring that the business remains compliant and financially sound.

Long-term Tax Planning and Strategy

Long-term tax planning involves more than just preparing for the upcoming tax season. It requires a strategic approach to financial management, considering future investments, potential business expansion, and changes in tax legislation.

This proactive approach helps minimize future tax liabilities and supports business growth.

Staying Informed and Proactive

In the ever-evolving landscape of tax law, staying informed and proactive is essential. Small business owners should continually educate themselves on new tax regulations and seek professional advice regularly.

This not only ensures compliance but also optimizes the business’s financial strategy for better growth and sustainability.